How I Evaluate Covered Call Trades (The Framework I Use)

- Chuck Shmayel

- Mar 6

- 5 min read

A lot of discussions around covered calls focus on a single variable such as implied volatility or delta. In practice, good covered call trades usually come from several positive factors aligning at the same time.

Covered calls are not simply about selling premium. The goal is to structure a position where each possible outcome is acceptable. The process starts with the stock itself and then works through the option characteristics and trade structure.

Start With the Underlying Stock

The most important rule of covered calls is simple: only sell calls on stocks you are comfortable owning. The option premium is secondary. The stability and quality of the underlying stock is the foundation.

Stocks that tend to work well for covered calls usually have strong liquidity, tight bid and ask spreads, and active options markets with high volume and open interest. They should also have reasonably stable fundamentals and no major unresolved risks.

Covered calls typically perform best when the stock is neutral to slightly bullish. A stock that is collapsing can overwhelm the premium collected, while a stock in a strong breakout can move through the strike quickly and cap upside too early.

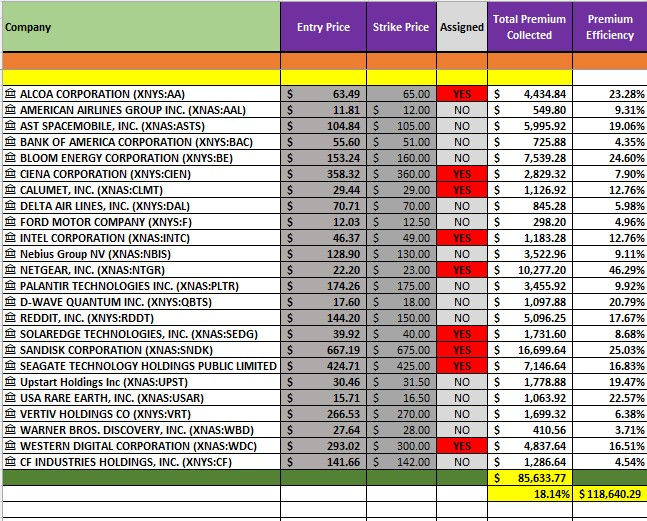

To help with stock selection I built the CCR list. It screens thousands of symbols using multiple filters specifically designed for covered call setups. The goal is to narrow the universe to stocks where the premium, liquidity, and probability profile make sense for covered call sellers.

Delta and Assignment Probability

Delta is one of the most useful metrics when choosing a strike price because it approximates the probability that the option finishes in the money and gets assigned.

Typical ranges I use are:

0.25 to 0.35 delta

Lower assignment probability with smaller premium.

0.40 to 0.55 delta

A balanced approach between income and assignment probability.

0.60 and higher

Higher income potential but assignment becomes more likely.

Delta helps define the probability profile of the trade before it even starts.

Premium Yield

Premium should always be evaluated relative to the stock price. A simple way to do this is by calculating the premium yield.

Premium Yield = Option Premium ÷ Stock Price

For example, if a stock trades at $100 and the option premium is $3, the premium yield for that cycle is 3 percent.

For roughly thirty day option cycles, premiums in the 2 to 5 percent range tend to be attractive. When premiums fall below that range the trade often becomes less efficient relative to the capital required.

Implied Volatility

Implied volatility plays a major role because it directly impacts option pricing. Higher volatility typically produces higher option premiums.

Selling calls when volatility is elevated or expanding often leads to better income opportunities. At the same time extremely high volatility can signal increased uncertainty, so it should always be considered alongside the quality of the underlying stock.

Timing the Entry

Entry timing can improve premium capture. Selling calls on up days often produces better pricing because both stock price and option demand increase.

Selling into strength when a stock approaches resistance levels can allow traders to capture stronger premiums while maintaining a reasonable probability of assignment.

Option Liquidity

Option liquidity is another important element that sometimes gets overlooked.

Good covered call candidates usually have strong open interest, consistent daily options volume, and tight bid and ask spreads. Liquid options markets help reduce slippage and make it easier to adjust or roll positions if needed.

Strike Distance

Strike distance also affects the structure of the trade. Many traders select strikes slightly out of the money, often a few percent above the current stock price.

This approach allows for some upside participation while still collecting meaningful premium income.

In-the-money calls provide larger premiums but increase the likelihood that the shares will be called away.

Earnings Timing

Another factor worth watching is earnings timing.

If an earnings announcement occurs during the option cycle the stock can move significantly. Some traders avoid selling calls during earnings unless the premium justifies the additional risk.

Trend Alignment

Trend direction can also improve the quality of a covered call setup.

Covered calls often perform better when the underlying stock is stable or trending upward. Stocks trading above longer-term moving averages or showing consistent trend signals tend to provide more reliable environments for the strategy.

Return If Called

One metric that helps evaluate the full trade is the total return if the shares are called away.

Return if Called Percentage =

(Strike Price minus Stock Price plus Premium) divided by Stock Price

For example:

Stock price $100

Strike price $105

Premium $3

Return if called equals 8 percent for that cycle.

This calculation includes both the stock appreciation and the option premium.

Expiration Timeframe

Expiration selection also matters.

Weekly options decay quickly but usually provide smaller premiums and require more frequent management.

Many covered call traders prefer option cycles around thirty to forty five days because they balance premium income, time decay, and flexibility.

Return on Investment

Return on investment depends on the outcome of the trade.

If the call expires worthless, the premium becomes the realized income while the shares remain in the portfolio.

Example:

Stock position $5,000

Premium received $200

ROI equals $200 divided by $5,000, or 4 percent for that cycle.

If the call is assigned, the profit includes both the premium and the stock appreciation.

Example:

Stock $50

Strike $55

Premium $2

Profit equals $2 premium plus $5 stock gain, or $7 total.

The return equals $7 divided by $50, or 14 percent.

The Mindset Behind Covered Calls

The key idea behind covered calls is that assignment is not a failure. It is simply one of the designed outcomes of the strategy.

The trade should be structured so that all three scenarios are acceptable.

If the stock stays flat, the premium is collected.

If the stock rises, the shares may be called away at a profit.

If the stock declines, the premium provides some downside cushion.

The goal is to combine strong underlying stocks, reasonable probabilities, and attractive premium income so that the trade works across multiple market outcomes.

The CCR list helps simplify the first step by filtering thousands of stocks down to candidates where the premium, liquidity, and probability characteristics are aligned with covered call strategies.

Educational disclaimer:

This content is for informational and educational purposes only and does not constitute financial or investment advice. Options involve risk and are not suitable for all investors. Covered calls limit upside potential and still expose investors to downside risk in the underlying stock. Always conduct your own research or consult a licensed financial professional before making investment decisions.

This response has been verified and cross-checked using four AI platforms to deliver a well-rounded, high-confidence perspective.

Comments