Why “Premium Collected” Is the Wrong Performance Metric

- Chuck Shmayel

- Feb 25

- 3 min read

I’ve been seeing more conversations lately around “monthly income” from covered calls — screenshots of premiums collected, annual income projections, and yield claims based purely on option sales.

And honestly… it’s been bugging me.

Because focusing only on premium is one of the most misleading ways to measure covered call performance.

The real question isn’t:

“How much premium did you collect?”

The real question is:

“What return did you generate on the capital deployed to produce that premium?”

That’s where the Covered Call Research (CCR) framework shifts the lens.

The CCR Measurement: % Distance From Strike

Instead of anchoring performance to premium dollars, CCR measures % distance from strike — because that represents the structural return embedded in the contract if assignment occurs.

Example:

Stock price: $100

Call sold: $103 strike

Distance from strike: 3%

That 3% is the foundational return for the cycle.

Premium sits on top — but the strike distance defines the capital gain component if shares are called away.

In CCR thinking, assignment isn’t a failure.

It’s a planned exit.

Translating Strike Distance Into Real Returns

Now let’s annualize that structure.

If you’re running monthly cycles:

3% return per cycle

× 12 cycles per year

That equates to:

~36% annualized return

Factor in premium density, occasional roll credits, and redeployment timing — and you’re realistically operating in the ~40% capital velocity range under consistent conditions.

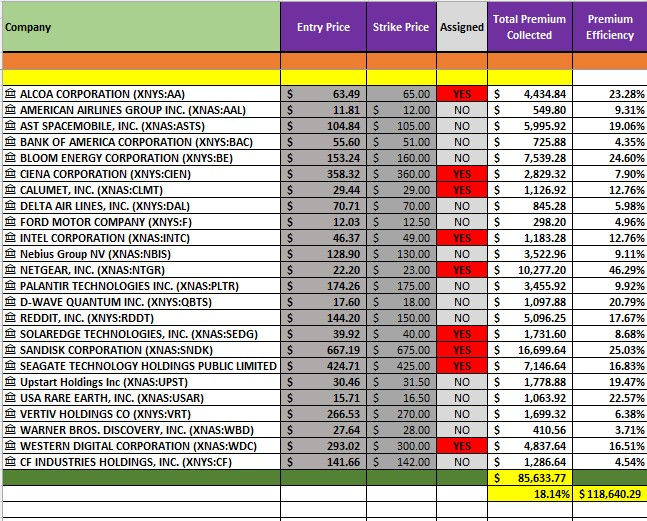

That’s a dramatically different performance picture than simply saying:

“I collected $800 this month.”

Because $800 means very little without context.

If it required $25,000–$50,000 in tied-up capital, the yield efficiency may actually be mediocre.

The Full CCR Performance Stack

CCR evaluates covered call performance through four integrated lenses:

1) % Distance From Strike

Primary return engine — defines structural yield if assigned.

2) Premium % of Stock Price

Income enhancer — boosts cycle yield but isn’t the core driver.

3) Assignment Probability

Determines exit likelihood and capital turnover timing.

4) Redeployment Speed

Controls compounding — how fast capital gets recycled into the next trade.

When you measure all four together, the strategy stops being “monthly income”…

…and becomes cycle-based capital yield management.

Busy vs Efficient Capital

This is where many traders have their wake-up moment.

You can generate large premium totals…

…but still run an inefficient book.

Example realization:

Collecting $800 in premiums isn’t impressive if $25K+ was tied up to produce it.

CCR analysis often reveals which tickers are:

Efficient yield producers

vs

Simply “busy” premium generators

That distinction drives better allocation decisions, strike selection, and redeployment discipline.

The Mindset Shift

When you adopt the strike-distance lens:

You stop asking:

“How much income did I make?”

And start asking:

“How hard did my capital work this cycle?”

That shift separates casual call sellers from structured income operators.

Covered calls move from being a side hustle…

…to becoming a capital strategy.

Educational Disclaimer

This content is provided for informational and educational purposes only and should not be construed as financial, investment, tax, or legal advice. Options trading involves risk and is not suitable for all investors. Covered call strategies can limit upside potential and may result in assignment of shares at the strike price.

All examples, scenarios, and return illustrations are hypothetical and used strictly to explain strategy mechanics — they are not guarantees of future performance. Market conditions, volatility, liquidity, and individual execution can materially impact outcomes.

Always conduct your own due diligence and consider consulting with a licensed financial professional before implementing any options strategy.

Comments